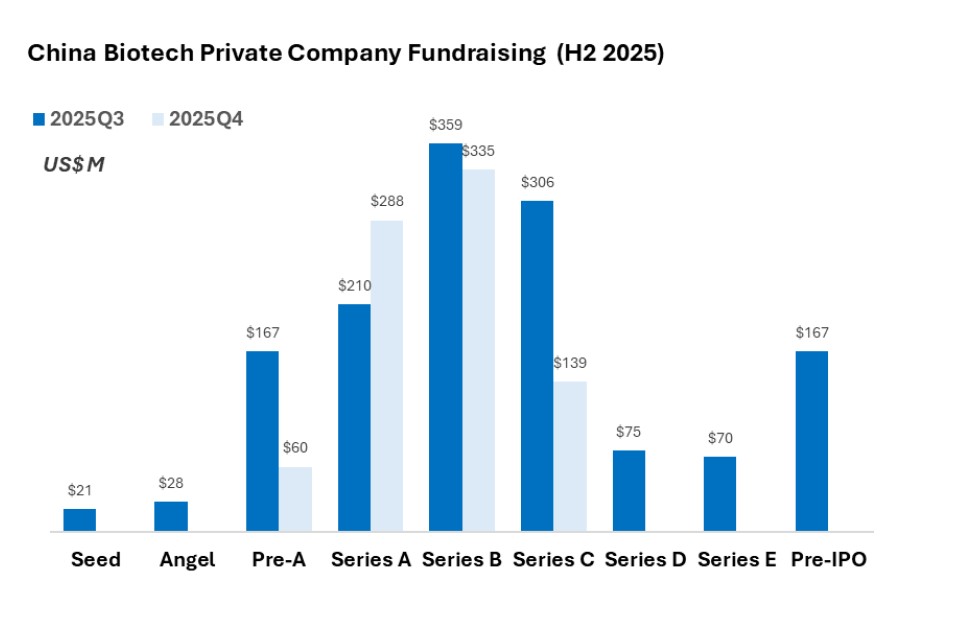

China Biotech private financing in H2 2025 reflected a distinct “flight to quality,” moving from the valuation outliers of Q3 toward a disciplined clinical focus in Q4. As Dr Cathy Bi of PharmaBoardroom content partner Selesta writes, while early-stage deal volume cooled, strategic liquidity remained robust for assets with mature clinical data or specialized modalities like ADCs and RDCs. Total disclosed financing for the final months of the year reached approximately US$ 1.02 billion, concentrated in high-barrier platforms and late-stage clinical advancements.

Investment Summary: The Shift Toward De-risked Assets

The narrative of H2 2025 is one of selective aggression. Investors concentrated capital into “mega-seed” rounds for platforms with high technical barriers while demanding clear exit pathways for late-stage investments.

- Q3 Capital Concentration: The third quarter was defined by extreme capital density in select assets. Outlier valuations were seen in early-stage firms like Accuredit Gene (US$75M Series A) and VelaVigo (US$ 60M Pre-Series A+), signaling a “mega-seed” trend for veteran-led platforms.

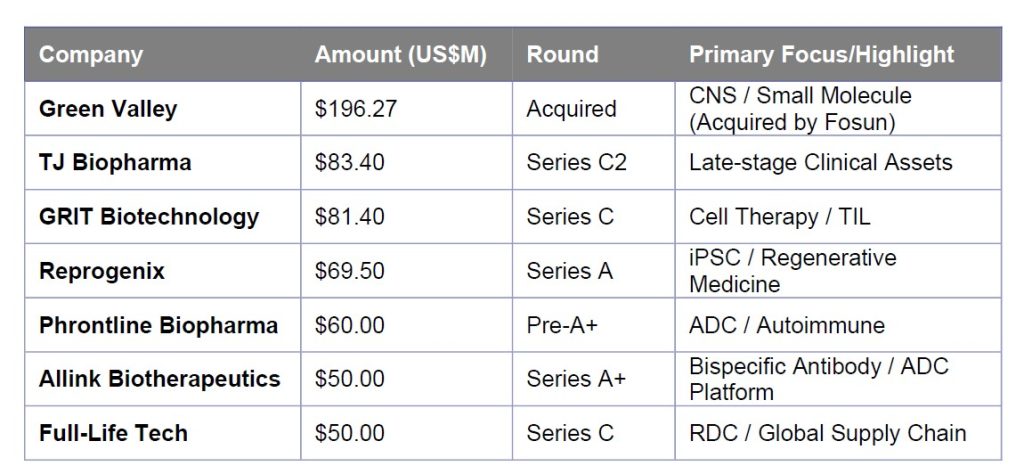

- Q4 Market Normalization: Activity shifted toward established players. The standout deal of the quarter was TJ Biopharma’s US$ 83.4M (RMB 600M) Series C2, underscoring a preference for companies with late-stage clinical or commercial capabilities.

- The ADC/RDC Multiplier: Antibody-Drug Conjugates (ADCs) remained the primary theme for large-scale deployment (e.g., the US$ 950M LaNova acquisition). Simultaneously, Radiopharmaceuticals (RDCs) showed unique resilience, evidenced by Full-Life Technologies’ US$ 50M Series C.

Key Financing Activity (Oct–Dec 2025)

The following table highlights the strategic focus on clinical-stage assets and high-moat technologies during the year-end normalization.

Sector Themes and Analyst View

The “Mega-Seed” Trend vs. Early-Stage Cooling

Q3 was characterized by early-stage companies commanding late-stage check sizes, bypassing traditional valuation curves. However, by Q4, this cooled significantly, with fewer disclosed Series A rounds of significant size. We view this not as a lack of capital, but as a deliberate pivot toward disciplined consolidation.

Modality Resilience: ADCs

The market remains “open” for ADCs due to their high technical barriers and global potential. The US$ 950M LaNova acquisition in Q3 provided a strong liquidity signal, supporting high valuations in this sub-sector through year-end.

Regional Hubs of Innovation

Funding remained concentrated in established biotech clusters. Shanghai, Hangzhou, and Suzhou dominated the deal flow, benefiting from mature ecosystems and state-owned capital support (e.g., Shanghai State-owned Capital Investment in Vitalgen).

Disclaimer

This report is prepared by Selesta Partners Limited for informational purposes only and is intended exclusively for the recipient. It does not constitute financial advice, endorsement, or solicitation. Selesta assumes no responsibility for the accuracy or completeness of the information provided, which is subject to change due to market or regulatory factors. Unauthorized use, distribution, or reproduction of this report is prohibited and may result in legal action. Recipients should seek independent financial advice before making investment decisions and are solely responsible for evaluating risks. Past performance is not indicative of future results, and this report does not guarantee any outcomes. By accessing or using this report, you acknowledge and agree to these terms.

This piece was originally published on the Selesta website here