John Murphy, III, president & CEO of the Association for Accessible Medicines (AAM) lays out a stark warning: the very medicines that keep the US healthcare system affordable and functioning are at risk. Generics and biosimilars fill nine out of ten prescriptions yet account for a tiny slice of spending, and new AAM–IQVIA data shows the market pressures threatening their survival. Murphy argues that the time has come for policymakers to realign before the backbone of American healthcare starts to buckle.

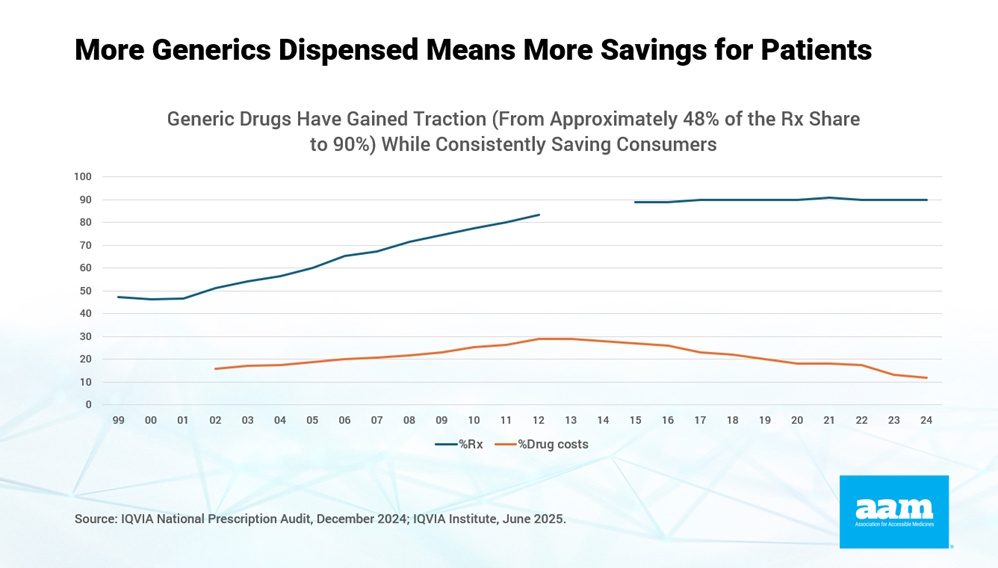

In the US in 2024, generic and biosimilar medicines comprised 90 percent of all prescriptions filled, but only 12 percent of prescription spending. In sharp contrast, brand drugs supported patients less often – making up only 10 percent of prescriptions filled but adding up to 88 percent of the total drug spend. In other words, Americans spent only USD 98 billion filling 3.9 billion generic prescriptions and a whopping USD 700 billion filling just 435 million brand drug scripts. More impressive, though, might be that the total amount spent on generic prescriptions in the same year accounts for only 1.2 percent of all US healthcare spending. This enormous impact at such a minimal relative cost proves the generic medicines industry is truly the backbone of the US healthcare system; however data within AAM’s 2025 US Generic & Biosimilar Medicines Savings Report clearly exposes fractured market conditions, and an industry that could be crushed without swift and purposeful action.

Here’s the clear truth: generic medicines are the only sector that consistently result in decreased spending across the US healthcare ecosystem. In fact, since 2019, the amount spent on all generic sales in the US has declined by USD 6.4 billion, despite increased volume and new generic launches.

For over a decade, AAM has partnered with The IQVIA Institute to capture relevant data and help describe the value of generic and biosimilar medicines in the US. Despite the hype and the discussion about drug pricing, the data shows an alarming but consistent trend. And, unfortunately, it has been this way for the last decade. Since 2016, generic drugs have steadily made up 9 out of every 10 prescriptions filled, all the while their overall percentage of costs has declined – from 27 percent in 2016 to only 12 percent in 2024.

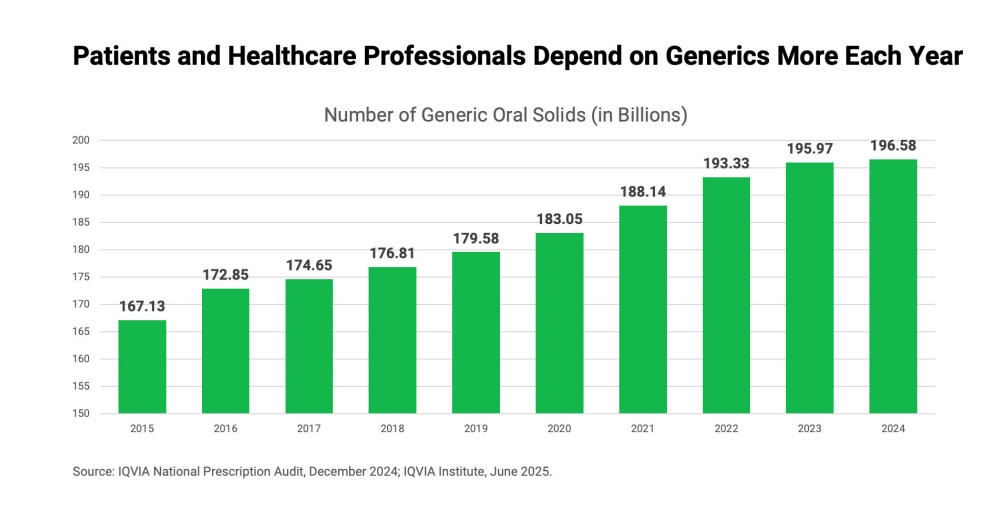

Does this mean the number of available generic drugs has decreased? No! Americans are relying on increased quantities of lower-priced, high-value medications. As noted in the graph below, with respect to generic oral solids (i.e., pills and capsules), the overall trend is an increased number of these products being prescribed and sold. In 2015, the total number of generic oral solids was approximately 167 billion. Within a decade (in 2024), that number increased to approximately 197 billion – a 15 percent increase. Over ten years, Americans were prescribed and received nearly two trillion generic oral solids. Keep in mind, this figure does not include a host of other products made by generic manufacturers (e.g., injectables, creams, etc.).

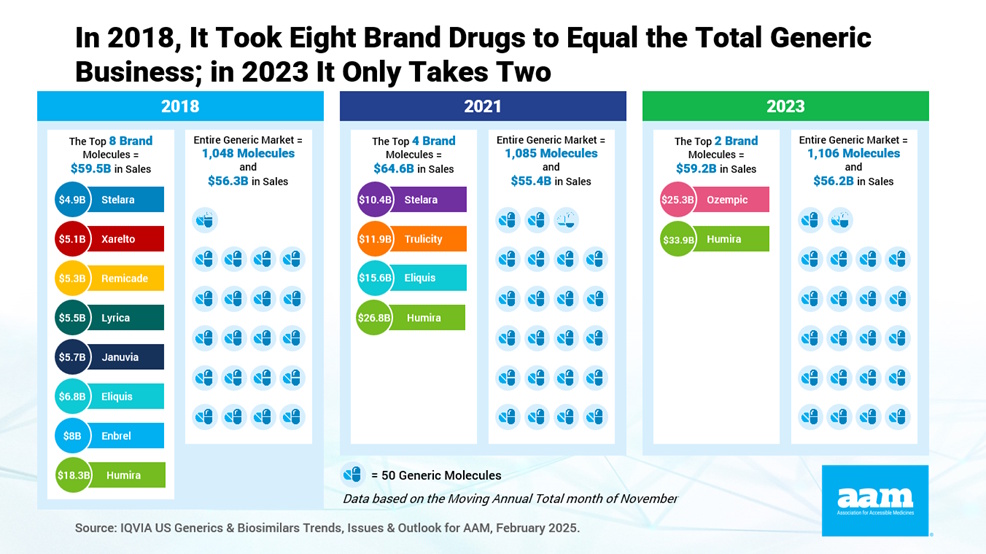

So, the question becomes: Why are drug prices still increasing? While the overall price of generic medicines is consistently dropping, the overall price of brand drugs is consistently increasing. In fact, in 2018, the amount spent on eight different brand products equalled the total US spending on ALL generic products. But flash forward to 2023 and we learn the sum of the amount spent on just two branded products – Ozempic and Humira – was greater than the total spent on 1,000 generic drugs combined.

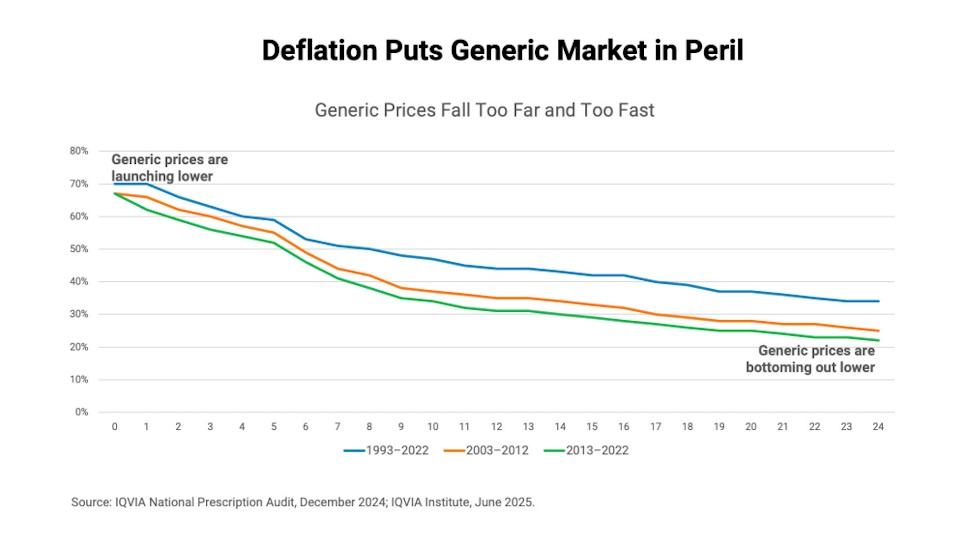

Perhaps most concerning is that, right now, little is being done to infuse sustainability into the generic medicines marketplace. As noted in the graph below, compared to 30 years ago, generic drugs are launching at lower prices and bottoming out at lower prices. The biggest change has been increased savings through the use of generic drugs. Three decades ago, generic prices tended to stabilise at approximately 34 percent of the brand product’s list price. But in the last decade, that percentage has continued to drop – to 22 percent. This type of deflation induces unsustainable market conditions for generic drug manufacturers and, sadly, dangerously impacts the ability of America’s patients to receive affordable care.

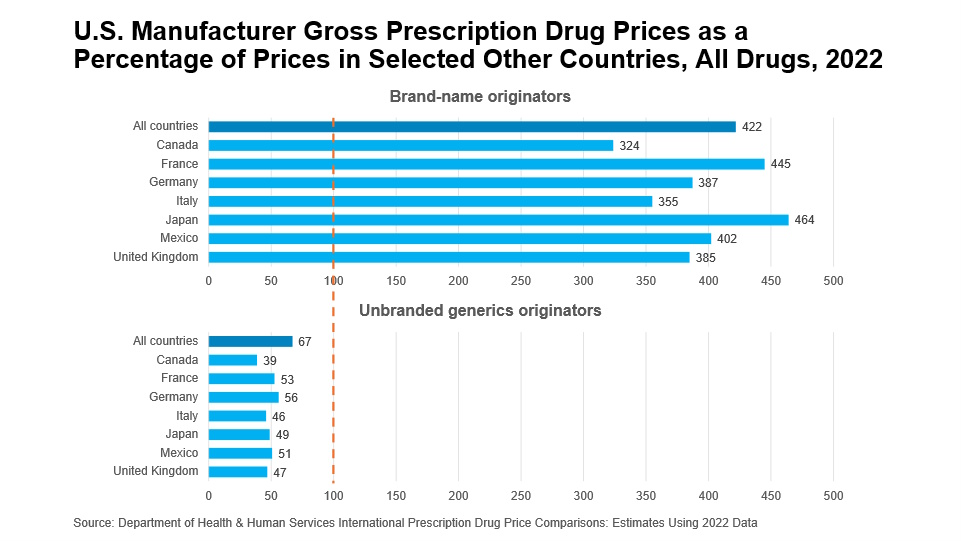

When it comes to potential solutions, we know that government-imposed price-setting is not the best answer. With Most Favored Nation (MFN) lingering around as a buzzword for prescription manufacturing stakeholders – both in Washington, DC and across the globe – I think it’s more important now than ever to separate generic and biosimilar medicines from brand drugs and originator biologics. Let’s look at a recent report from HHS, in partnership with RAND Health Care and with access to IQVIA data, as an example of why. In the US, patients pay more for brand drugs than in any other developed country in the world. In fact, US prices for brand-name drugs cost an average of 422 percent more than the same drugs in comparison countries. But this is simply not the case for generic medicines. On an international scale, generic medicines in the US cost less – a lot less. The same HHS report found that Americans pay about 67 cents to the dollar for generic medicines, when analysed against the 33 comparison countries.

Thankfully, there has been a recent and historic shift in US trade policy – one that reflects the growing recognition of our industry’s essential role in public health through a sustainable global ecosystem of players. Billions of dollars in new investments that exponentially increase domestic manufacturing of generic medicines have been recently announced by AAM member companies and I’m certain we will see more domestic investment on the horizon. I am thrilled to see that when it comes to trade policy, the uniqueness of our industry is starting to sink in in Washington. For the first time in recent history, the brand and generic medicines industries are being treated differently – and very rightly so. For example, we’ve now seen finalised trade deals in Europe that protect free trade for generics and biosimilars while imposing tariffs on brand-name products.

All said, I think most experts would agree that the best single word to describe the generic and biosimilar medicines industry is complex. But this doesn’t mean we cannot be described as strong, too. This is because solutions that infuse sustainability and protect access to treatments for patients who depend on medicines to thrive are not too far out of reach. I urge policymakers to take the steps necessary to infuse stability into arguably one of the most important industries to public health and US national security. Now is the time to align on AND push through policies that roll back harmful federal mandates – including IRA price controls; to streamline FDA processes; to curb patent abuse; and to stop PBMs and Medicare from denying patient access. And the urgency of this matter impacts us all – because without generics and biosimilars, 90 percent of prescriptions in Americans’ medicine cabinets would disappear.